Rishi Sunak has said there is a “deep moral responsibility” to get inflation under control as the cost-of-living remains stubbornly high.

The prime minister’s characterisation came as official data on Wednesday showed inflation defied expectations that it would slow and held at 8.7% in May – making the rate of price growth in Britain the highest of any major economy once again.

It means the Bank of England is likely to hike interest rates again on Thursday in a desperate attempt to cool the economy down, spelling bad news for homeowners who face further increases in mortgage repayments. The central bank’s over-arching aim is to keep inflation at 2%.

Sunak vowed in January that the government would halve the rate at which prices are rising by the end of the year. At the time, the inflation rate was around 10%.

Speaking at an event on Thursday, Sunak will put an added emphasis on the goal.

He is expected to say: “I feel a deep moral responsibility to make sure the money you earn holds its value.

“That’s why our number one priority is to halve inflation this year and get back to the target of 2%.

“And I’m completely confident that if we hold our nerve, we can do so.”

His comments suggest lowering inflation now trumps economic growth – one of Sunak’s other promises – which could have other negative economic impacts.

Acknowledging that this is a difficult time for families and businesses, the prime minister will add: “Beating inflation has to be the priority … because if we don’t get a grip on inflation now, the damage will be worse and longer lasting.”

The UK has an inflation problem. Officials had hoped the rising cost of goods and services would have been brought to heel by now, as soaring energy costs fuelled by the war in Ukraine have cooled.

The Office for National Statistics said inflation, as measured by the consumer price index, held steady at 8.7 per cent in the year to May. Expectations were that the rate would fall a to 8.4 per cent.

Advertisement

And there was more. Britain’s measure of underlying inflation that excludes volatile items, such as energy and food, took investors by surprise by accelerating for a second month in a row in May, hitting 7.1 per cent, up from 6.8 per cent in April. Higher core inflation is seen as a sign that price growth is more likely to remain persistently high.

<img class="img-sized__img landscape" loading="lazy" alt="UK inflation remains unchanged at 8.7% in May.” width=”720″ height=”693″ src=”https://www.wellnessmaster.com/wp-content/uploads/2023/06/so-why-exactly-is-inflation-higher-in-britain-than-in-the-us-and-europe-2.jpg”>

UK inflation remains unchanged at 8.7% in May.

Anadolu Agency via Getty Images

It looks certain that the independent Bank of England will raise the cost of borrowing again on Thursday for the 13th month in a row – the only question is whether it’s by 0.25 percentage points, or a symbolic half percentage point to 5%.

Don’t other countries have inflation under control?

Britain’s inflation rate has stayed far above price growth in the US and elsewhere in Europe. Although 8.7% is down from a peak of 11.1% last October, it leaves the UK with the highest inflation rate among the G7 advanced economies. By comparison, inflation stood at 4% in the US and 6.1% across the 20 EU countries that use the euro currency.

Advertisement

Last week, the Federal Reserve – America’s equivalent of the Bank of England – ended a 15-month streak of hiking interest rates, a pause that currently seems highly unlikely in the UK.

The surging cost of food

Britain has had western Europe’s highest rate of inflation for food, with prices up more than 18 per cent over the past year, down only slightly from a recent peak of more than 19 per cent, the highest since 1977.

Freak weather has affected crops around the world, pushing up prices for many countries. But Britain is the world’s third largest net importer of food and drink, according to the Food and Agriculture Organisation of the United Nations – behind only China and Japan – leaving it particularly exposed.

Industry data published on Tuesday showed British grocery inflation eased slightly for the third month in a row in June.

Bank of England governor Andrew Bailey said last month that British food producers may have locked in higher costs than the central bank had anticipated, explaining some of its underestimate of inflation.

Advertisement

Heavy reliance on natural gas

Britain is highly reliant on imported gas to generate electricity, exposing it to the full force of the surge in gas prices last year after Russia’s invasion of Ukraine.

The way Britain regulates energy prices for domestic and business users – it announces changes to maximum tariffs on a quarterly basis – means that international price rises are slower to push up inflation than in many other countries but falls are also slower to feed through into bills for users.

Brexit

Exiting the European Union and its single market at the start of 2021 has started to have an impact. Although an agreement between the UK and the bloc allows largely tariff-free trade in goods, there are barriers to exports and imports in the form of paperwork which have caused delays and higher costs.

Meanwhile, the end of free movement of workers from EU countries has contributed to an acute shortage of staff for many employers, pushing up wages and ultimately prices for consumers.

Bank of England decision-making

Some economists think the Bank, which is tasked with keeping inflation at around 2%, was too slow in starting to raise interest rates and is now playing catch-up.

Advertisement

Its own monetary policy committee rate-setter member, Chaterine Mann, said in February that the Bank should have started raising interest rates earlier (“a greater degree of front-loading” was needed) and is now paying the price.

Chancellor Jeremy Hunt will hold a meeting with Britain’s major banks on Friday to discuss how they can help homeowners hit by rising mortgage costs, after saying the government would not offer borrowers significant financial help.

The Bank of England has raised interest rates 12 times since December 2021, but the impact for many mortgage holders is only starting to be felt now as low fixed rates agreed during the Covid-19 pandemic start to expire.

Advertisement

Some politicians have called on the government to consider financial aid for those worst hit, but Hunt rejected this in a parliamentary question-and-answer session.

“We won’t do anything that would mean we prolonged inflation,” Hunt said when asked about possible aid. “Schemes which involve injecting large amounts of cash into the economy right now will be inflationary.”

Conservative MP Jake Berry asked Jeremy Hunt whether it was time to consider mortgage interest relief at source. Jeremy Hunt also told MPs that he will meet mortgage lenders about what relief they can offer to their customers.https://t.co/MN45tfGyF1pic.twitter.com/T0hlw2V3Sy

The Bank of England is expected to raise interest rates again on Thursday by a quarter point to a 15-year high of 4.75% in a bid to fight unexpectedly sticky inflation, which was running at 8.7% in April. Official inflation data for May will also be published on Wednesday.

Advertisement

Hunt said he would talk with major lenders later this week to discuss the challenges faced by some borrowers.

Three sources – two from the banking industry and one in the government – said that meeting would take place on Friday and focus on how best to support customers facing big increases in their repayments this year, and those who have refinanced at higher rates and are already struggling to cope.

“I’ll be meeting the principal mortgage lenders to ask what help they can give to people struggling to pay more expensive mortgages and what flexibilities might be possible for families in arrears,” Hunt said.

The 2008 financial crisis did not lead to a big wave of home repossessions in Britain, but lending rules were tightened afterwards to ensure homebuyers taking out mortgages would still be able to cope with a significant rise in interest rates.

However, mortgage rates have risen rapidly in recent weeks as markets bet the BoE may have to raise its own interest rate as high as 6% next year to tackle persistent inflation.

Advertisement

Trade body UK Finance estimates 800,000 Britons will need to refinance loans in the second half of this year, and a further 1.6 million in 2024.

The Resolution Foundation think-tank estimated that the average homeowner who refinances a mortgage in 2024 will have to pay an extra £2,900 pounds a year.

Most British residential mortgages have interest rates fixed for two or five years, after which borrowers pay a floating rate or switch to a new fixed rate.

It’s the 12th increase in a row since rates started going up in December 2021, pushing borrowing costs up further, particularly impacting homeowners with a mortgage.

Soaring food prices – and the fact they remain stubbornly high – appears to be the key factor behind the decision.

Advertisement

But experts are not sure it’s the right policy

Some economists think the Bank could has gone too far since the impact of the repeated rises has yet to pass through to households and businesses.

Take homeowners. Around 85% of all borrowers are tied to fixed-rate mortgages – but the majority are yet to switch to a higher-rate home loan, and could be in for a shock when they do.

One prominent commentator predicted “screeching U-turns are coming” – and the Bank will soon have to cut rates to avoid tipping the UK economy into recession.

So how do interest rates work?

Hiking the base rate increases the cost of borrowing, making both credit and investment more expensive. The idea is to put the brakes on the economy and curb the soaring cost of goods and services – known as inflation.

Advertisement

Bringing rates down is an attempt to have the opposite effect – stimulate growth by making borrowing cheaper, and in turn, encourage investment.

The Bank is tasked with keeping inflation under control, targeting 2% a year. Inflation hit 10.1% in March, and raising rates is the blunt instrument it has to bring it down.

This is the bind the Bank is in: raise interest rates to combat inflation, but then stall the economy and make people’s lives miserable and make any downturn potentially deeper and longer.

Why are experts calling it out?

Put simply, some economists argue that pushing up rates is having little to no effect on inflation – mainly because the war in Ukraine has been the driving force, chiefly through higher energy costs that are now easing. The same applies to two other factors, namely higher oil prices and economies emerging from a pandemic.

Consumer champion Martin Lewis suggested on Twitter that the Bank was sending signals more than anything else. Lewis wrote: “I’m no economist, but I struggle with the logic behind base rate rises currently. Inflation seems supply-side driven – but rate rises dampen demand. Then again the BoE is charged with bringing down inflation and this is it’s only tool. So it has to do it. Co-ordinated effort with govt would help.”

Advertisement

I’m no economist, but I struggle with the logic behind base rate rises currently. Inflation seems supply-side driven – but rate rises dampen demand.

Then again the BoE is charged with bringing down inflation and this is it’s only tool. So it has to do it. Co-ordinated effort…

David “Danny” Blanchflower, who sat on the Bank’s monetary policy committee for three years, accused the central bank of “terrible incompetence”.

“The consequences of raising rates are much worse than the cost of inflation”.

Former member of Bank of England Monetary Policy Committee, Professor Danny Blanchflower responds to another interest rate rise saying it is “complete incompetence”.https://t.co/0UDPc82y6hpic.twitter.com/y5s6RhgxOo

“This is utter incompetence. The market doesn’t believe them. I don’t believe them.

“I don’t believe a word that they say and it’s going to make things much worse for your listeners.

“Housing market’s going be in trouble. Mortgages are going to go up, housing quantities are going to decline.

“It’s the same utter group-think incompetence in 2008, and the same bank missed the greatest financial crisis since 1929.

“And here they go again. The market doesn’t believe them. I don’t believe them.

“Your listeners shouldn’t believe them. Screeching u-turns are coming and bad economic data is coming.

“This is terrible incompetence and this lot should just quit.”

Others were of a similar mind.

Suren Thiru, economics director at the Institute of Chartered Accountants in England and Wales, said the Bank risked “overdoing” rate rises, which could compound the cost crisis for many.

Advertisement

He said: “With most of the interest rate rises yet to pass through to households and businesses, the Bank of England risks overdoing the rate hikes, adding to the squeeze on our growth prospects and aggravating the cost-of-living crisis.”

The IPPR think tank argued the Bank should have held off raising interest rates again, warning of a “continued increase in inequality”.

Carsten Jung, senior economist at IPPR, said: “The Bank of England should have held off raising rates.

“The current approach risks creating big economic costs, in the form of lower future growth and fewer jobs, while not actually being effective enough at bringing down inflation.”

What does the Bank say?

The Bank had previously been more optimistic that inflation could fall as low as 1% by the middle of 2024, but it is now predicted to reach about 3.4%, meaning it will fall at a significantly slower rate.

Advertisement

Andrew Bailey, the Bank’s governor, said there had been a “very big underlying shock” to food prices.

He added: “It appears to be taking longer for food price pressures to work their way through the system this time than we had expected.”

“But, as we said before, we are in very unusual times.”

Britain needs to stop playing “pass-the-parcel” with someone accepting that they are poorer to get inflation under control, the chief economist of the Bank of England has said.

Huw Pill said that people and businesses have responded to higher bills and costs by asking for higher wages or charging their customers more money.

Advertisement

But households and companies trying to pass on their higher costs, he said, adds to inflation, pushing up prices even further across the economy.

UK inflation – the measure of the rising cost of goods and services – hit 10.1% in the year to March. It was a fall from 10.4% in February, but still remains stubbornly high – and above the 9.8% that experts had predicted.

The Bank of England is tasked with keeping inflation under control, targeting 2% a year.

Speaking on the Beyond Unprecedented podcast from Columbia Law School, Pill said: “The UK, which is a big net importer of natural gas, is facing a situation where the price of what you’re buying from the rest of the world has gone up a lot, relative to the price of what you’re selling to the rest of the world, which is mainly services in the case of the UK.

“You don’t need to be much of an economist to realise that if what you’re buying has gone up a lot relative to what you’re selling, you’re going to be worse off.

Advertisement

“So, somehow in the UK, someone needs to accept that they’re worse off and stop trying to maintain their real spending power by bidding up prices whether through higher wages or passing energy costs on to customers etc.

“What we’re facing now is that reluctance to accept that, yes, we’re all worse off and we all have to take our share; to try and pass that cost onto one of our compatriots and saying, ‘we’ll be alright, but they will have to take our share too’.

“That pass-the-parcel game that’s going on here, that game is one that’s generating inflation, and that part of inflation can persist.”

A former Bank of England policymaker has said that the UK economy has been “permanently damaged” by Brexit, because it reduced the country’s potential output and resulted in reduced investment into UK businesses.

In an interview on Bloomberg TV, Michael Saunders said that Jeremy Hunt’s “austerity budget” this week is a consequence of leaving the EU.

Advertisement

Saunders joined the rate-setting Monetary Policy Committee shortly after the Brexit referendum in 2016, and left the role in August this year.

He said: “The UK economy as a whole has been permanently damaged by Brexit. It’s reduced the economy’s potential output significantly, eroded business investment.

“If we hadn’t had Brexit, we probably wouldn’t be talking about an austerity budget this week. The need for tax rises, spending cuts wouldn’t be there if Brexit hadn’t reduce the economy’s potential output so much.”

Advertisement

This message needs to be repeated loudly and often. Brexit is ONE OF the causes of the pain that will be felt by everyone as austerity bites. To turn things around, it will be necessary (but not sufficient) to join the single market and customs union. We need to face reality. https://t.co/UMsvhW2api

On Sunday, Hunt denied that Brexit has made the UK poorer – despite the government’s own Office for Budget Responsibility saying it has.

The chancellor, who campaigned for Remain in the 2016 referendum, insisted the UK can make a “tremendous success” of leaving the EU.

He said it is important to consider the effects of Brexit “in the round”, and that Brexit brings both “costs” and “opportunities”.

The chairman of the OBR, Richard Hughes, last year said that Brexit would reduce the UK’s potential gross domestic product by 4% in the long term.

Advertisement

Saunders, who is now senior economist at Oxford Economics, added some of the ambitions behind Liz Truss’s failed mini-budget were correct in that “raising potential output is the big challenge”, but her “suggested solution to cut taxes and deregulate are wrong”.

He added: “I put the emphasis more on improving trade links with the EU, improving education, training, and also fixing this worrying rise in long-term sickness, which has been reducing the workforce so much.”

Saunders said the economy has faced a “challenging period with the Brexit vote, the depreciation of sterling, a long period of political uncertainty, the pandemic and then renewed political uncertainty”.

Last week, former Bank of England governor Mark Carney doubled down on his claims the move has taken a toll on the pound, suggesting the decision to leave the EU continues to play a part in the UK’s financial woes.

Jacob Rees-Mogg has taken aim at the independent fiscal watchdog that analyses government budgets despite the huge market unrest.

On the day the pound plunged again, the business secretary trashed Office for Budget Responsibility (OBR) forecasting and even suggested chancellor Kwasi Kwarteng could ignore them if they were overly negative.

Advertisement

OBR assessments of the UK economy will accompany the chancellor’s plan to pay for his economic measures and reduce debt on October 31.

A lack of such forecasts during last month’s seismic mini-budget are thought to have contributed to the recent chaos in financial markets – with the cost of government borrowing soaring and the Bank of England forced to intervene.

In a pre-recorded interview on ITV’s Peston, the cabinet minister said: “Let’s see what the Office for Budget Responsibility has to say rather than guessing what it may say.

Advertisement

“But its record of forecasting accurately hasn’t been enormously good.

“So, the job of chancellors is to make decisions in the round rather than to assume that there is any individual forecaster who will hit the nail on the head…

“There are other sources of information. The OBR is not the only organisation that is able to give forecasts.”

His comments are unlikely to reassure investors seeking a firm commitment from the Government to get the nation’s finances under control.

Rees-Mogg also lashed out at the International Monetary Fund (IMF) after it called for the UK’s economic support package to be more targeted and for fiscal policy to be tightened.

He said: “I think the IMF is wrong on both counts. I think it’s particularly wrong on energy, and frankly doesn’t know what it’s talking about…

Advertisement

“The IMF is not holy writ and the IMF likes having a pop at the UK for its own particular reasons. I’m afraid I would never lose too much sleep about the IMF.”

This is exactly what we’ve seen since the mini-budget – Ministers repeatedly going out making things even worse with foolish comments further undermining confidence in the UK.

While they’re in power everyone will pay a premium on their mortgage https://t.co/mBCd0uIQy0

Earlier, the senior Conservative accused Today programme presenter Mishal Husain of failing to meet the BBC’s impartiality standards after she suggested the mini-budget had unleashed the market turmoil.

Labour’s shadow chief secretary to the Treasury Pat McFadden said: “Even now, Tory cabinet ministers do not appear to have learned lessons since their disastrous mini budget.

“The more they publicly trash economic institutions like the OBR, the more they undermine market confidence in their plans and their management of the UK economy.

“The Tories are out of control and working people are being made to pay the price with higher mortgage payments.”

Financial experts have roundly rejected the business secretary’s analysis that interest rates were to blame for the market turmoil.

Gillian Tett, Financial Times US editor-at-large, told Channel 4 News: “To use a non-technical term, that’s pretty much bollocks.”

A Financial Times journalist has offered a withering assessment of the government’s suggestion that the Bank of England is to blame for the recent chaos in the markets.

On Tuesday, business secretary Jacob Rees-Mogg suggested the central bank’s failure to raise interest rates in line with the US was driving the financial turmoil rather than chancellor Kwasi Kwarteng’s mini-budget.

Advertisement

But Gillian Tett, the FT journalist who made her name for her prescient commentary on the 2008 financial crash, has said – bluntly – that this was really not the case.

Appearing on Channel 4 News, and asked for a verdict, Tett said: “To use a non-technical term, that is pretty much bullocks.

“I think for the most part it really was the budget and the way it was delivered and the message inside, which sparked the beginning of the crisis.

“The Bank of England certainly is to blame for not having prepared for these kinds of dislocations. The British pension funds appear to have been somewhat asleep at the wheel in terms of their risk management systems.

Advertisement

“But at the end of day, the spark that lit this fire was very much the budget announcement.”

Earlier, Rees-Mogg argued the market response was “much more to do with interest rates than it is to do with a minor part of fiscal policy”.

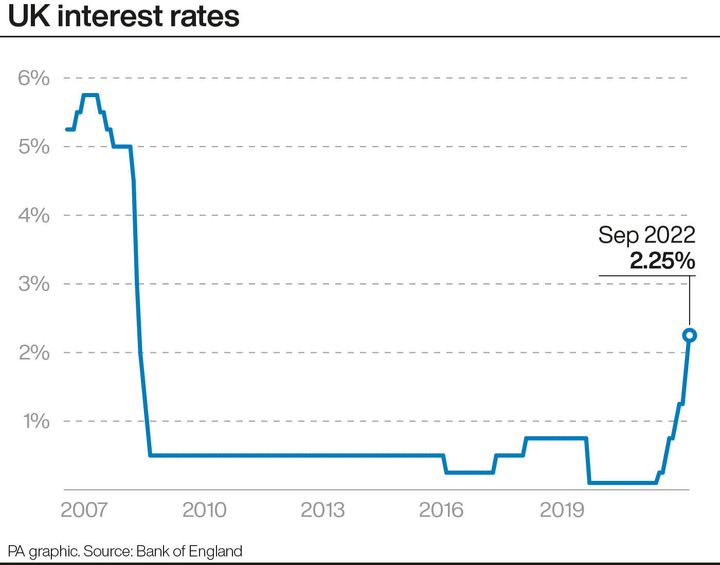

On September 22 the Bank’s Monetary Policy Committee (MPC) raised rates by 0.5 percentage points to 2.25%, but the day before the Federal Reserve raised rates by 0.75 percentage points.

But economists insisted that the government’s decision to increase borrowing without any plan to balance the books was a major factor.

The cost of government borrowing increased on Wednesday while sterling fell against the euro and dollar in the latest signs of market turbulence.

The governor of the Bank of England made clear its emergency support programme for the county’s fragile bond market will end on Friday – sparking another sell-off of the pound.

Andrew Bailey warned pension fund managers “you’ve got three days left” to balance the books as the central banker made clear efforts to shore up the financial markets had to be temporary.

Advertisement

It’s almost two weeks since the Bank launched a massive programme to help pension funds cope with a slump in bond prices triggered by the announcement of unfunded tax cuts by the new Liz Truss government.

Earlier on Tuesday, it made a fresh attempt to soothe market chaos, enacting another round of emergency bond-buying after a renewed bout of market turbulence.

Investors have been selling-off government bonds – also known as gilts – as investor concerns about the state of the British economy has failed to subside.

Following the announcement by the governor, the pound plunged against the dollar to below $1.10.

Spooked by the biggest raft of tax cuts for half a century, the pound fell to its lowest point ever against the dollar following the mini-budget – dropping to just over $1.03 – but has rebounded since in no small part thanks to the Bank’s efforts.

Advertisement

Gosh Just look at what happened to the pound when @bankofengland Governor Andrew Bailey told investors its emergency support will definitely end on Friday. “You’ve got three days left now,” he said. “You’ve got to get this done.” pic.twitter.com/ij9verfBBW

At an event organised by the Institute of International Finance in Washington on Tuesday, Bailey said: “We have announced that we will be out by the end of this week. We think the rebalancing must be done.

“And my message to the funds involved and all the firms involved managing those funds: You’ve got three days left now. You’ve got to get this done.”

Earlier on Tuesday, the Pensions and Lifetime Savings Association, an industry body, urged the BoE to extend the bond-buying programme until October 31 “and possibly beyond”.

Advertisement

Why has the Bank stepped in with more emergency action?

On Tuesday, the Bank said it needed to broaden the emergency programme to buy UK government bonds to calm markets as it warned over a “material risk to UK financial stability”.

Advertisement

It came after a further sell-off in the gilt market, which saw the yields on long-dated government bonds rise back up close to levels seen in the immediate aftermath of the mini-budget.

What are gilts and gilt yields?

UK government bonds are a way for the government to raise money.

A gilt is essentially an IOU that the Treasury writes to its lenders, promising to pay the money back, plus interest, within a time frame, for example over two, 10 or 30 years.

The yield on a gilt is the amount of money an investor receives for owning the debt and is represented as a percentage of its price. When a bond price falls, its yield rises.

Yields rise when investors are less willing to own the debt, meaning they will pay a lower price for the bonds.

Why are bond yields rising?

Concerns over the chancellor’s plans for unfunded tax cuts sent gilt yields soaring as markets fretted over the Government’s economic policies.

Advertisement

At one stage, the yield on 30-year gilts hit levels not seen since 2002 in the chaos that followed the mini-budget statement, while the pound also plunged to record lows against the US dollar.

What do gilt prices have to do with pension funds?

Pension funds invest huge amounts of money in gilts, which are seen as safe investments in usual times.

In order to protect themselves against sharp rises in government borrowing costs, funds have been investing in products that act as a kind of insurance – so-called liability driven investment (LDI) funds.

But due to the sudden rise in government borrowing costs after the mini-budget, investment banks called on these LDIs to put up assets or cash as securities for loans, which in turn called on pension funds, forcing them into a fire sale of gilts, driving prices still lower and yields higher and creating a downward spiral.

How bad is the latest crisis in financial markets?

The Bank warned last week that it had been been forced to step in to avoid market meltdown, when some pension funds were left close to collapse and there was a risk of a knock-on impact elsewhere in the financial system.

Advertisement

Its measures initially eased pressure on gilt yields, but they spiked higher again and there are signs the woes may be spreading elsewhere, to index-linked gilts, as well as corporate bonds and even in niche debt markets in the US.

Will my pension be affected?

Experts say the gilt rout, which is largely affecting final salary and defined benefit pensions schemes, will not impact policyholders.

The Pensions and Lifetime Savings Association (PLSA) said: “Although there has been a great deal of commentary over the last few weeks, members of defined benefit pension schemes should be reassured that their pension benefits are safe; scheme funding is strong and, despite the operational challenges, funding will have been strengthened further by rising yields.”

Why are mortgage rates rising?

Higher gilt yields and the prospect of rising interest rates as the Bank looks to cool rampant inflation have a significant impact on mortgage lenders.

Rates on two and five fixed year deals have gone past 6% for the first time in many years due to the market turmoil, while lenders have also been pulling hundreds of products.

Advertisement

Will the latest action be enough?

There are concerns that when the Bank’s programme comes to a close on October 14, there will be a further sell-off of gilts, leaving pension funds in chaos once more.

The PLSA has called for the bond-buying programme to be extended to the chancellor’s next fiscal statement on October 31 or even beyond, suggesting there may yet be further intervention from the Bank.

The language of economics and the financial system can be confusing for those not steeped in the world of pensions, gilts and bear markets.

But there’s been a lot of around, as the Conservative Party’s mini-budget spooked the markets, causing a collapse in the pound and a surge in the UK’s borrowing costs. Here’s an explanation to some of the phrases and ideas being bandied around.

Advertisement

Why is ‘supply-side economics’ being mentioned?

The economic theory is highly fashionable having been fully embraced by the UK’s new prime minister, Liz Truss and her chancellor, Kwasi Kwarteng, in their controversial “fiscal event”.

The theory holds that the supply of goods and services within the economy is the main driver of growth. Put bluntly, the idea is to give wealthy individuals or large corporations tax cuts, which in turn creates jobs and later increases the number of people paying taxes and boosts the amount of money collected by the Treasury. The prime minister’s approach has been dubbed “Trussonomics”, and supporters talk a lot about baking a bigger economic “pie” that everyone can share.

The theory was particularly popular in right-wing circles in the 1980s. In common with US president Ronald Reagan, UK prime minister Margaret Thatcher experimented in this kind of low-tax economics, the results of which have been disputed ever since.

<img class="img-sized__img landscape" loading="lazy" alt="Chancellor Kwasi Kwarteng arrives at Darlington station for a visit to see local business.” width=”720″ height=”482″ src=”https://www.wellnessmaster.com/wp-content/uploads/2022/09/a-guide-to-the-confusing-language-describing-the-uks-financial-markets-meltdown-3.jpg”>

Chancellor Kwasi Kwarteng arrives at Darlington station for a visit to see local business.

Owen Humphreys via PA Wire/PA Images

Advertisement

The phrase “trickle-down” economics – the benefits generated at the top trickling down to everyone – has become synonymous with the idea.

When talking about supply-side economics, commentators will invariably refer to the Laffer Curve – a graph showing the relationship between tax rates and the amount of tax revenue collected by governments. It’s named after Arthur Laffer, a member of Reagan’s economic policy advisory board, who also advised Thatcher, earning him the nickname the “father” of supply-side economics.

When do we know we’re in a recession?

A technical recession is defined by two successive quarters of falling economic output – measured by gross domestic product (GDP), which attempts to summarise all the activity of companies, governments and individuals in an economy in a single figure.

Some people argue the term “recession” is an unreliable indicator because people could be suffering all the effects of an economic downturn, such as long-term unemployment, but the data might not officially say as much.

Kwarteng has admitted the UK is “technically” in a recession, even if the official figures are yet to confirm it.

Advertisement

In 2020, the Office for National Statistics (ONS) officially declared the UK in recession – the steepest on record – after the economy plunged by 19.6% between April and June due to the coronavirus lockdown.

It followed a 2.2% contraction in the previous three months – marking the first recession since the 2008 global financial crisis, when the UK fell into a year-long recession.

What is inflation?

At its heart, inflation is the measure of how quickly the cost of goods and services is growing. It is an average across many categories, so if food prices rise, that could still be offset by drops in, say, the price of petrol.

In the UK, the ONS is tasked with estimating the inflation rate.

It has a basket of goods and services that it tracks. It might be helpful to think of this as a massive shopping basket with what the ONS thinks that people in the UK buy. It includes around 730 items, anything from dating agency fees to condoms, wild bird seed to petrol, and crumpets to pet food.

What is in the basket changes every year – with some additions and some removals – because what people buy changes. For 2022 antibacterial surface wipes were added, along with meat-free sausages and other items.

Advertisement

What’s the Bank of England’s role?

Owned by but independent from the UK government, the Bank of England is tasked with keeping inflation under control, targeting 2% a year.

But in recent months inflation has started to run away. It hit 9.9% in August and, despite government action to freeze energy bills, is still expected to strike a new 40-year-high “just below 11%”, the central bank has said.

The Bank of England also has a wider remit to ensure the health of the economy. Many will remember the economy-boosting stimulus in the form of quantitative easing – often referred to as printing money – being deployed during the 2008 financial crisis.

How do interest rates fit in?

An interest rate is a measure that tells you how high the cost of borrowing money is, or how high the rewards are for saving.

Advertisement

The Bank of England’s “base rate” – the interest rate at which banks borrow from the central bank, which has billions of pounds in assets at its disposal – has a knock-on effect on the interest rates offered on the high-street for mortgages and savings.

Raising and lowering interest rates is the blunt instrument at the Bank’s disposal to control the economy. Hiking the base rate increases the cost of borrowing, making both credit and investment more expensive. The idea is to put the brakes on the economy and curb soaring inflation. Bringing rates down is an attempt to have the opposite effect – stimulate growth by making borrowing cheaper, and in turn, encourage investment.

UK interest rates. See story ECONOMY Rates. Infographic PA Graphics. An editable version of this graphic is available if required. Please contact graphics@pamediagroup.com.

PA Graphics via PA Graphics/Press Association Images

Before the mini-budget, the Bank raised the base rate by 0.5 percentage points – the seventh hike since December – in a bid to keep inflation under control. Now some analysts are predicting the base rate, currently standing at 2.25%, will have to rise to as high as 6% next year.

What about bonds and yields?

The Bank of England has also intervened to try to bring surging yields in government bonds – known as gilts – under control as they spiralled higher, sending UK public borrowing costs soaring.

Advertisement

It said it would buy bonds “on whatever scale is necessary”. The Bank stepped in to calm markets after some types of pension funds were at risk of collapse.

Bonds are loans that investors make to a bond issuer and can be issued by companies or governments to raise money.

The yield on a bond is the amount of money an investor receives for owning the debt and is represented as a percentage of its price. When a bond price falls, its yield rises.

Yields fall when investors are less willing to own the debt, meaning they will pay a lower price for the bonds.

Alarm bells were ringing when yields on 10-year UK government bonds rose above 4%, the highest since the 2008 financial crisis, and more than triple the 1.3% rate at the start of the year.

Advertisement

The higher yield reflected fears investors had in the state of the UK economy, and again impacts how much interest banks charge for various types of loans, most notably mortgages.